It’s easy and fun and you can do it at home on this site in your pajamas!

But first, think about 5 ways to figure out how much life insurance you need these questions to see if it even makes sense for you to consider life insurance.

Do you find yourself lying awake at night worrying about what could happen if tragedy strikes?

Will your family be able to pay their bills? What would happen to your outstanding debts without enough term life?

Will your child be able to go to college if you were gone and don’t have enough life insurance?

These are tough questions to think about, but finding the answers are critical to picking the right term life insurance policy.

Oh, and if you think that men are the only people who need life insurance, think again! Women need life insurance as much, or even MORE than men due to their increasing equality in the workplace…

Quick Navigation

Basic Life Insurance Terms

Premium

Beneficiary

Evidence of Insurability

Life expectancy

Policyowner

Types of life insurance

Term Life Insurance–The Magic Bullet!

Universal Life Insurance–If You Really Feel Like Wasting Your Money

Whole Life Insurance–It’s Like A Model-T Ford

Do You Even Need Life Insurance?

5 Steps To Figuring Out How Much Life Insurance You Need

Online life insurance calculators

We understand that figuring out the right amount of life insurance to carry (or if you should have life insurance at all) can be a tricky question to answer, and we’re here to help! In the following post, we will help you make sense of your situation by clearing up some misconceptions about life insurance, the three types of plans available and their benefits, and finally a five-step process you can use to calculate the size of the policy you need.

Let’s start with some definitions of key terms and a basic description of life insurance to make sure that we’re on the same page.

Basic Life Insurance Terms

It’s Like A Foreign Language!

Beneficiary

The person named by the policy owner to receive the proceeds from the insurance policy once the policy owner is deceased.

Evidence of Insurability

Proof of your health, and finances or job, to help the insurer determine your risk.

Life expectancy

The probability of someone living to a certain age based on specific mortality tables. Calculating life expectancy is the first step to determining the true cost of life insurance and is reflected in the basic premium.

Policyowner

The individual that enters into an agreement with an insurance company for a life insurance policy.

Types of life insurance

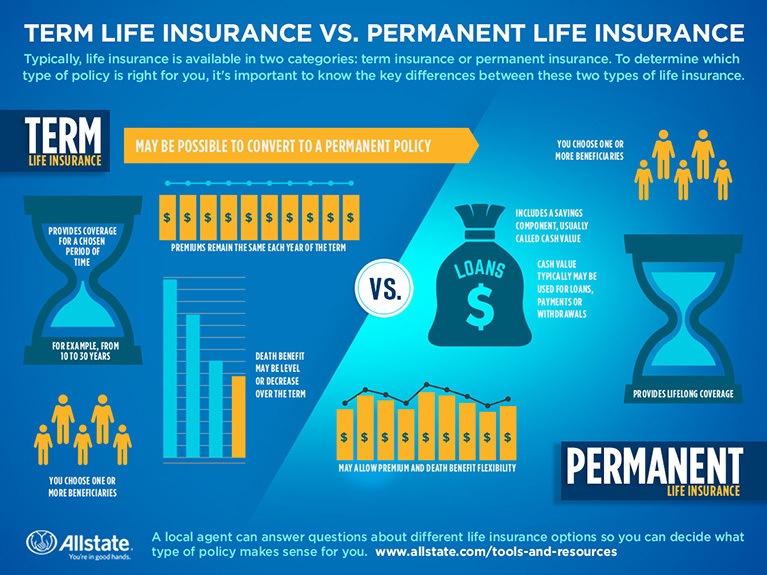

Term Life Insurance–The Magic Bullet!

Life insurance is much like any other insurance policy. In essence, you enter into an agreement with an insurance provider for coverage in exchange for a payment or premium every month, quarter, or year. While auto insurance covers you in case, you get in an accident and health insurance covers your medical expenses if you go to the hospital, life insurance will provide your beneficiaries with a lump-sum payment in the event of your death.

Death is a difficult subject to discuss for many people, but it is important to have a plan in place in case the worst happens. Especially as you age, life insurance becomes more and more essential in most cases, and making sure you are prepared should be your number one priority.

Like any insurance, life insurance is more complicated than “sign here, and you’re covered.”

There are multiple types of life insurance policies each with their own benefits and drawbacks. Here are the most common life insurance policies and their benefits:

Term life insurance offers protection for a set period of time.

This period could be around 10 to 20 years and is suitable for replacing a lost potential income during your working years since it provides a safety net for your family and helps keep your financial goals such as paying off your mortgage on track.

Traditionally, premium payments stay the same for the entire term.

Once the term is finished, insurers can choose to offer continued coverage for the policy owner, however at a higher premium payment.

Term life insurance is usually a more cost-effective choice compared to permanent life insurance as well since it is only for a set period of time.

Term life insurance is a good choice for someone that is still working, but the sole provider for their dependents.

Universal Life Insurance–If You Really Feel Like Wasting Your Money

The following two are worth taking a look at if you want a long-term policy solution. The first, universal life insurance, is a permanent life insurance policy that usually offers flexibility in premiums. Throughout the life of the policy, you can choose to lower or raise your premiums or coverage amounts to best fit your needs at the given time. However, keep in mind that universal life insurance typically comes with a higher premium payment than term life insurance.

Many choose universal life insurance when planning a flexible estate to help preserve wealth and provide the maximum amount of benefits to beneficiaries once the policy comes to an end. Universal life insurance may also be utilized as a long-term income replacement for beyond the policy owner’s working years.

Whole Life Insurance–It’s Like A Model-T Ford

Henry Ford built great cars, but these days they are better off in museums and car shows. Same with Whole Life Insurance!

Whole life insurance is designed to provide coverage for the policy owner’s lifetime.

There are usually higher premiums under a whole life insurance policy because of the extent of its coverage, and these premiums are generally set at a fixed price. Whole life insurance has a cash value that can function as a savings tool that accumulates tax-deferred wealth over time.Whole life insurance is a great tool to use when planning an estate as it helps preserve your wealth when transferring to your beneficiaries.

Do You Even Need Life Insurance?

The short answer–probably. Why else are you searching the internet for life insurance quotes?

However, it depends.

If you are 22 years old, single, and don’t carry a significant amount of debt, you don’t need to worry about life insurance for a while. The biggest benefit of being covered under a life insurance policy is the ability to support your beneficiaries in the event of your untimely death.

However, if you are in your later years, have a family that depends on you, or carry a significant amount of debt compared to assets, life insurance is crucial to securing a stable financial future for your family once you are gone. Without being covered, your family could be stuck trying to pay for your death expenses (funeral, cremation, etc.) along with supporting themselves. Nobody wants that for their survivors, so purchasing a life insurance policy of some sort is crucial.

5 Steps To Figuring Out How Much Life Insurance You Need

You might have heard about the “rule of thumb” for determining the right amount of life insurance coverage you should carry.

This rule is known to be around seven to ten times your yearly income. While this number can be helpful when estimating the amount of coverage you need, you really should try to calculate the exact amount so you can rest easy knowing that your beneficiaries will be completely covered should tragedy strike.

Below are five steps you can follow to get a reasonably good estimate of the amount of coverage you need as well as the type of plan that might be right for you.

1. When looking at your personal finances, how much debt do you have not including your mortgage? If you have any debts other than your mortgage, the chances are that you are operating at a negative net income, meaning that you are spending more than you earn. Because of this, you will need life insurance to help pay off this debt if the unexpected happens.

2. Take a look at your bank statements or a personal budget software tool and figure out roughly how much money you are spending each month. This is vital to determining how much your family will need once you are gone so don’t guess here! At first glance, $500,000 worth of coverage might seem like more than enough, but you could be wrong.Here is a quick example to determine how much life insurance you might needIf your family were to receive a $500,000 lump-sum in the event of your death and invest the full amount, they could make around $25,000 through a simple diversified portfolio in one year. If your salary is around $25,000, then a $500,000 policy might be right for you. If your salary is more than that, then you would need to purchase a larger plan.

3. How much are you putting away each month? If you are good at saving money each month and live within your means, first of all, keep it up, and secondly, you might not need a policy which covers your entire salary since you have accumulated wealth over time that can pay off your debts.

4. Do you have long-term savings goals you would like to meet? Examples of this could be saving for retirement, a future car purchase, or college tuition for your children. You don’t want death to derail your plans for your beneficiaries so be sure to consider these savings goals.

5. The only thing that really matters when it’s all said and done is how much income your beneficiaries will need. You must answer this question before finally deciding on the right policy for yourself. Total your answers from the previous steps and you should have a fairly exact figure.

Along with these five steps, there are also tons of online life insurance calculators that can help you do the math. A few sites other than this one worth looking into include:

Calculate Your Needs – Life Happens

Bankrate Life Insurance Calculator

Timing Is Key when buying life insurance

You may have heard that it is harder to qualify for life insurance as you get older compared to when you are younger. This is a myth that many insurers perpetuate as part of their tactic to convince you to sign up for life insurance as soon as possible. Insurance companies make their money by betting on how long their policy owners will live, so they stand to make more from younger policyholders than they do from older policyholders.

The younger the policy owner, the longer they are likely to live, so insurers can keep collecting monthly premiums without much risk. If a young policy owner were to die unexpectedly, then the insurer will take a hit. Since this is less likely, insurers are willing to take their chances and try to accumulate as many younger policy owners as possible.

The fact of the matter is that if you have the financial means to afford the monthly premiums, you can qualify for life insurance at any stage in life, and the decision of when to sign up is completely up to you.

That being said, there are instances when it is smarter to sign up for life insurance when you are younger. If there are people that depend on you, you should take out a life insurance policy in case disaster strikes. Without it, your loved ones could be thrust into financial uncertainty as they try to find a new way to support themselves. It is recommended you purchase a term life insurance policy when you are younger because the premiums are lower and you are less likely to need the insurance, but it’s comforting to know that it’s there.

Another reason to purchase a life insurance policy in your younger years would be because you have a significant amount of debt compared to your assets. With a life insurance policy, you can be sure that if you were to pass unexpectedly, your debts would be resolved and your family would have a safety net to support themselves.

Can Life Insurance Be an Investment?

Yeah, a REALLY lousy investment!

Some types of life insurance policies can be utilized as investment vehicles in addition to providing you coverage for the unexpected. These plans are known as “cash-value policies” meaning they hold a cash value that can be invested with the insurance company, and you will earn interest on that investment which can be used to help you save for retirement or other expenses. While other investment strategies and vehicles can provide larger gains, investing in a cash-value life insurance policy takes a lot of the guess-work out of investing and doesn’t require much attention.

we’re here to help you in your search for the best life insurance policy for you and your family!

If you feel that now is the time to purchase a life insurance policy, contact us today, and we will work with you to find the best options that meet your needs along with the best plans available. We sincerely want all of our clients to feel confident that they’re ready for anything and that their loved ones are too.