Wouldn’t it be nice to wake up like this every morning knowing that you found the perfect term insurance policy- even with sleep apnea?

Wouldn’t it be nice to wake up like this every morning knowing that you found the perfect term insurance policy- even with sleep apnea?

Best Guide To Sleep Apnea Life Insurance [Updated 2026]

Wouldn’t it be nice to wake up every morning — refreshed, breathing normally, and knowing you scored a great rate on your term life insurance policy — even with sleep apnea?

Update: March 2026

A major 2025 study published in the European Heart Journal found that CPAP therapy provides measurable cardiovascular protection in high-risk obstructive sleep apnea (OSA) patients — particularly those with greater heart rate responses to respiratory events during sleep. The study of 3,549 participants found that CPAP-treated high-risk OSA patients had a notably lower rate of major adverse cardiovascular and cerebrovascular events compared to those receiving only usual care. In short: use your CPAP. Your heart — and your life insurance underwriter — will thank you.

“Our findings provide a much-needed basis for recognizing favorable long-term cardiovascular responses to CPAP for future prospective evaluations.”

— Study authors, European Heart Journal, August 2025

If you’re searching for sleep apnea life insurance, you’ll love this article.

There are a TON of other sites that merely “discuss” sleep apnea and give you a basic overview of the life insurance application process. One of my main competitors, Quotacy, has a popular blog post, but no others delve as deeply into the subject of sleep apnea life insurance as we do in this guide and on our entire site. Not even PolicyGenius or LifeInsuranceByJeff come close to going this deep into sleep disorders and life insurance.

And why would they? It takes a massive amount of time and research to come up with excellent resources on high-risk life insurance.

So, if you want detailed information on your condition, and the best possible guidance during the sleep apnea life insurance process, keep reading this guide. You may want to bookmark this page — it’s that detailed.

Let’s face it, sleep apnea is a pain in the neck. Literally and figuratively. So many more people have been diagnosed with it in the last 25 years that it’s now a huge industry. That also means that if you’ve been diagnosed with sleep apnea and you need life insurance, you’ll need someone to guide you through the process.

That’s exactly what I’ll do in this article. You’re not alone in this — I have moderate OSA and I “get it.”

Keep reading and you’ll get the most thorough information on sleep apnea life insurance available online. You’ll also get actionable steps you can take to get the lowest possible price on your life insurance.

Simply keep reading, and feel free to chat with us in the chat box if you have any questions!

Take care,

Chris

My Name Is Chris Acker, CLU, ChFC. I’m a life insurance broker — and I have sleep apnea. I was diagnosed with OSA in 2004. My AHI without treatment was 35. I started using CPAP in 2004 and my life changed! My current BiPAP device measures my AHI at about 2.5 each night. My life insurance company now loves me since I’m CPAP compliant!

More Than 80 Million Americans Suffer From Obstructive Sleep Apnea

According to a landmark 2025 study published in the journal SLEEP, an estimated 80.6 million individuals were living with OSA in the United States in 2024 — 59% male and 41% female. That’s a significant jump from the 54 million figure that was widely cited just a few years ago, and researchers say the number is nowhere near its peak. A separate 2025 Lancet Respiratory Medicine study projects that by 2050, OSA will affect 76.6 million U.S. adults aged 30–69, representing a nearly 35% relative increase from 2020 levels.

The problem remains that most people don’t know they have it. Their condition goes either undiagnosed or misdiagnosed. Only an estimated 10–20% of sleep apnea cases are ever formally diagnosed. They’re out there sleeping (badly) and blissfully unaware that their throat is staging a nightly mutiny.

Sleep apnea is also a major contributor to road accidents across the country. Drowsy driving causes at least 100,000 crashes, roughly 1,500 deaths, and billions in property damage annually. (Spoiler: falling asleep at the wheel rarely ends well — and it’s not great for your life insurance application either.)

Those Who Suffer From Sleep Apnea Often Have A Difficult Time Getting Good, Affordable Life Insurance

That’s why we’ve put this guide together — so you can navigate the sleep apnea life insurance maze without losing your mind (or your wallet).

In This 2026 Guide You’ll Learn:

- What Sleep Apnea Is And Why It’s Difficult, But Not Impossible, To Get Life Insurance

- What Sleep Apnea Does To The Body — Way More Than Just Snoring!

- How Sleep Apnea Is Treated And Why Life Insurance Companies Love CPAP Compliance

- Are There Any Permanent Cures For Sleep Apnea — What’s The Current State Of The Art?

- What Are Some Home Treatments For Sleep Apnea?

- What Type Of Doctor Should I See For Sleep Apnea?

- Totally Easy Steps You Can Take To Get The Best Rates On Your Life Insurance Application

- What AHI And RDI Readings Do Insurance Companies Want To See?

- Do I Tell My Life Insurance Company About My Sleep Apnea? (Yes. Always. We’ll explain why.)

- Don’t Have Your Life Insurance Application Declined For Non-Disclosure

- Who Has The Best Information To Help You Find The Right Policy?

What Is Sleep Apnea?

Sleep apnea is a sleep disorder characterized by repeated pauses in breathing, or periods of shallow breathing, during sleep. Each pause can last from a few seconds to a few minutes and happens many times per night. In its most common form, it’s followed by loud snoring — a sound that has ended more than a few marriages.

There Are Three Types of Sleep Apnea:

- Central sleep apnea (CSA)

- Obstructive sleep apnea (OSA)

- Mixed sleep apnea (both central and obstructive — overachievers only)

What Is The Life Expectancy Of Someone With Central Sleep Apnea (CSA)?

Central sleep apnea (CSA) occurs when the brain simply forgets to tell the body to breathe while you’re asleep. It’s rarer than OSA but significantly more dangerous. The estimated average lifespan of someone with untreated CSA can be shortened by up to 20 years compared to the norm. Causes can include brain infections, stroke, cervical spine conditions, severe obesity, and certain narcotic medications. The 2025 AASM Clinical Practice Guideline on Central Sleep Apnea recommends CPAP as the first-line treatment for most CSA subtypes — including heart failure-related and treatment-emergent CSA.

What Is The Life Expectancy Of Someone With Obstructive Sleep Apnea (OSA)?

People with moderate to severe OSA are 4x more likely to die when the disorder is left untreated. Uninterrupted sleep is essential for the body to repair itself. Fragmented sleep caused by OSA’s dysfunctional breathing patterns prevents the restorative rest the brain and body need — potentially leading to serious accidents, cognitive decline, and a long list of health complications that life insurance underwriters find very, very interesting (and not in a good way).

What Are The Consequences Of Untreated Sleep Apnea?

Sleep apnea has severe and life-shortening consequences if left untreated. It’s associated with:

- Heart disease and heart failure

- High blood pressure and stroke

- Type 2 diabetes and insulin resistance

- Depression, memory problems, and impotence

- Headaches and unexplained weight gain

- Drowsy driving accidents

In short: untreated sleep apnea is the gift that keeps on giving — and not in a good way.

What Is Continuous Positive Airway Pressure (CPAP)?

Continuous Positive Airway Pressure (CPAP) is the gold-standard therapy for sleep apnea. Patients wear a face or nasal mask during sleep connected to a pump that delivers a positive flow of air into the nasal passages to keep the airway open. It’s not exactly a fashion statement, but neither is a toe tag. CPAP wins. Learn more about CPAP and other treatment options at SleepApnea.org.

How Many Years Does A CPAP Machine Last?

Save money by maintaining your CPAP machine — your wallet will thank you when it comes time to pay your term insurance premium!

The average life expectancy of a CPAP machine is approximately 20,000 hours, or about seven to eight years of full-time use. A well-maintained machine has been known to last as long as 50,000 hours. Masks, however, wear out faster — for performance and hygiene reasons. The good news is that most health insurers provide replacement supplies on a regular schedule. Check with your insurer to see if you’re eligible.

Sleep Apnea Is Linked To Heart Disease — Life Insurance Companies Hate Co-Morbidity Factors!

A well-established body of research confirms that obstructive sleep apnea significantly increases the risk of heart failure and coronary heart disease, particularly in middle-aged and older men.

“Men with severe obstructive sleep apnea were 58 percent more likely to develop new congestive heart failure over eight years of follow-up compared to men without sleep apnea.”

— Dr. Daniel Gottlieb, Associate Professor of Sleep Medicine, Harvard Medical School

In 2025, a comprehensive multi-trial analysis published in the European Heart Journal confirmed that CPAP therapy — particularly with adherence of 4+ hours per night — significantly reduces cardiovascular risk in high-risk OSA patients. The analysis pooled data from 3,549 participants across three randomized trials and found that high-risk OSA patients on CPAP experienced 17% fewer major cardiac events compared to those receiving only usual care.

This is exactly why insurance companies care so much about whether you’re actually using your CPAP machine.

Sleep Apnea And Life Insurance Underwriting — Learn How It Works And What To Look For.

Pro Tip: Your Life Insurance Broker Should Know This Stuff. If Not, Find A New One!

People Suffering From Any Type Of Sleep Apnea Can Typically Get Some Form Of Life Insurance

Because obstructive sleep apnea is by far the most common type, it will be the main focus of life insurance underwriting. With an individual policy, OSA sufferers can typically get life insurance — provided you can demonstrate treatment compliance.

Unless you can document that your CSA condition was temporary or caused by environmental factors (like high-altitude sleep apnea, which resolves when you descend to lower elevation), central and mixed apnea cases face more limited options and may need to pursue group coverage through an employer or a guaranteed issue policy.

The standard underwriting scenario for treated OSA is standard life insurance rates. However, select companies may consider better rates if all other health factors are favorable.

How To Get A Sleep Apnea Life Insurance Policy Issued With The Best Possible Rates

What Does “Being Rated” For Life Insurance Mean?

A “rating” is a surcharge based on an expectation of higher claim expenses due to any medical condition, family history, or lifestyle. Sleep apnea will affect your rating and premium — especially if it’s paired with other conditions.

Key Factors Insurers Consider:

- Severity of your sleep apnea (AHI/RDI from your sleep study)

- Type of sleep apnea diagnosed (OSA vs. CSA vs. mixed)

- CPAP or other treatment compliance

- Co-existing conditions (obesity, diabetes, hypertension, high cholesterol, depression)

- Frequency of follow-up visits with your doctor

- Family medical history

When your sleep apnea is properly treated and controlled, it may not significantly affect your premium. In fact, modern CPAP technology like ResMed’s myAir app and similar platforms can document your compliance data precisely — and insurance providers are increasingly open to using that data in underwriting.

The Bottom Line: Insurance Carriers Want To See An AHI Of Less Than 5 — With Or Without A Corrective Device, CPAP, Or Surgery — To Consider You For “Preferred” Rates

If you can achieve this, combined with good vitals and a clean health history, preferred rates may be within reach. However, most people with sleep apnea also have multiple health conditions (the dreaded “co-morbidity” factors), and the more of those you stack up, the harder it is to hit preferred or standard rates.

Is Sleep Apnea Considered A Pre-Existing Condition For Life Insurance?

Yes. Several chronic respiratory disorders, including sleep apnea, are considered pre-existing conditions and may result in higher insurance rates. What’s more, one insurer in one state might accept an applicant with sleep apnea while another in the same state won’t. Every carrier is different.

According to Adam Amdur, Executive Director of the American Sleep Apnea Association:

“A diagnosis of sleep apnea can result in a ‘decline to cover’ by a life insurance company. If the insurance company does provide coverage, it will be at a much higher rate and with a limitation in the amount of coverage available.”

However — depending on severity and demonstrated management — you may qualify for standard or even better rates.

Could I Be Denied Insurance Because Of My Sleep Apnea?

Sleep apnea alone is rarely grounds for outright denial. However, if additional risk factors are present — obesity, high blood pressure, Type 2 diabetes — it could result in significantly higher premiums or a declination. The level of treatment you’re undergoing also matters enormously. If you can’t show that you’re actively treating your condition, expect an unfavorable decision.

Documentation That Helps Your Case:

- A recent sleep study report (polysomnography)

- Doctor’s notes showing diagnosis and treatment plan

- Proof of CPAP compliance

- Information on related health conditions (if any)

- Family medical history

Things All Sleep Apnea Sufferers Need To Consider When Choosing A Life Insurance Company

Not all carriers are created equal when it comes to OSA underwriting. Here are the critical questions your broker needs to be asking behind the scenes:

- Which life insurance carrier is most competitive for you today?

- Which insurer has an underwriter with the most experience with sleep apnea cases?

- Which company is more willing to be aggressive because they have sufficient reserves?

- Which company might be less aggressive due to reserve or credit concerns?

- Which carrier is under tighter control by their reinsurer?

- Which carrier is given more leniency by their reinsurer?

- Which carrier is hungrier for new business right now?

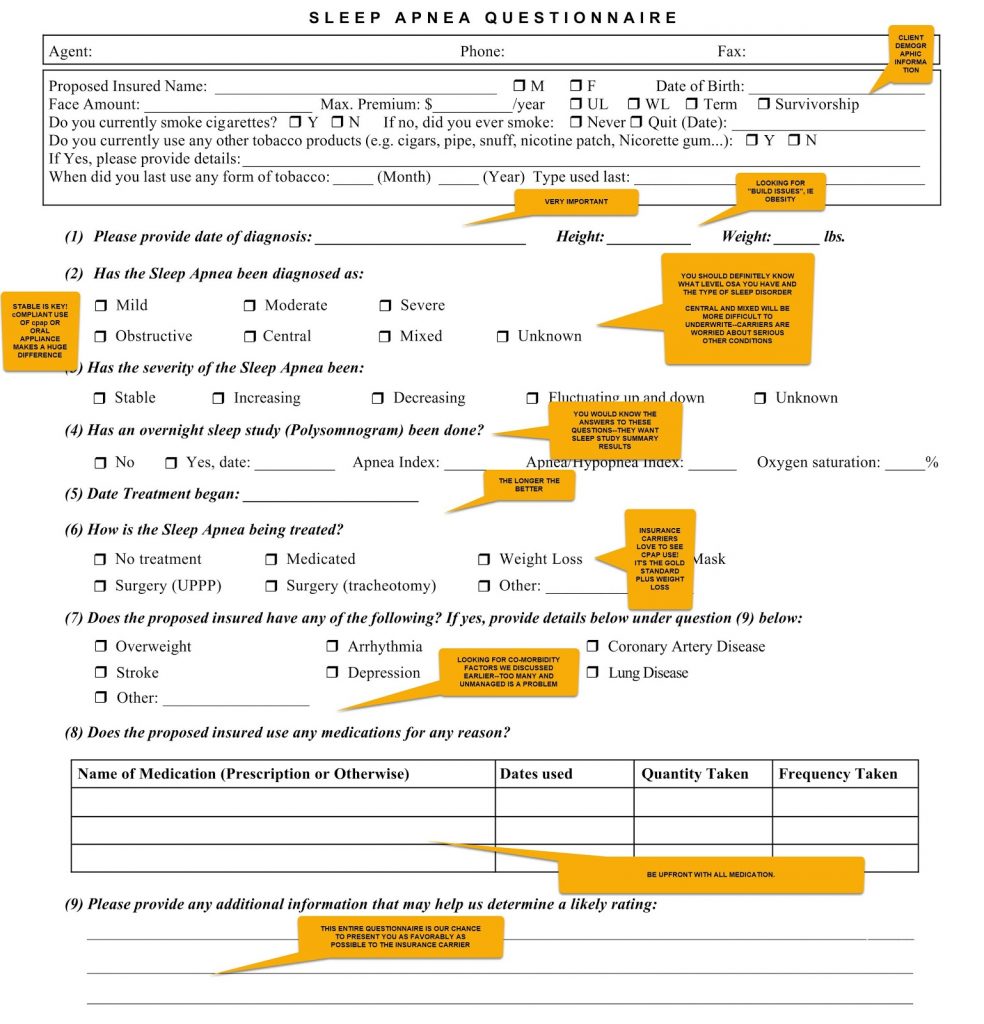

Life Insurance Sleep Apnea Questionnaire

Before your formal application goes to an underwriter, your broker needs to “field underwrite” your case — meaning they gather all the relevant details and present your situation clearly to a home office underwriter who can’t see or speak with you.

(Click on the photo to zoom into the annotations)

All of these factors come into play during underwriting. This is exactly why pre-qualification matters — your broker needs to test the waters and get a confident read on your likely rate class before you submit a formal application.

What Are The Best Life Insurance Companies For People With Sleep Apnea?

In our experience, the life insurance carriers that do the best job underwriting sleep apnea aren’t always the cheapest on a term insurance quote spreadsheet.

Some Insurers Are Better Than Others At Accommodating People With Sleep Apnea

If you see a “low-ball” or “teaser” rate on a term insurance website, dig deeper. Ask the broker whether those rates apply even with a history of OSA, CSA, or other major sleep disorders. You’ll often find the answer is a polite “no.”

Our recommended list of carriers with the best outcomes on sleep apnea life insurance applications is available when you call us directly. Carrier competitiveness shifts frequently, and what works best for you depends on your specific medical picture.

Make Sure To Use An Experienced Independent Life Insurance Broker Who Knows About Sleep Apnea And The Life Insurance Underwriting Process. You’ll Save Money And Time By Working With A Professional Who Knows The Market For Your Specific Health Condition!

What Research Is Being Done On Sleep Apnea Now?

The Tongue Fat Connection — Still A Big Deal

According to Dr. Richard Schwab, Professor of Sleep Medicine at the Hospital of the University of Pennsylvania, tongue fat remains one of the most significant focuses of cutting-edge sleep apnea research. His team’s landmark research established that in people with sleep apnea, approximately 32% of the tongue is composed of fat — compared to about 27% in obese people without sleep apnea.

A 2025 meta-analysis published in PMC confirmed these findings, concluding that tongue volume and fat are associated with the development of OSA independent of BMI — and called for larger studies to examine how targeted tongue fat reduction might offer new therapeutic opportunities.

And here’s the really practical finding: losing weight directly reduces tongue fat, which in turn reduces sleep apnea severity. In a Penn Medicine / NHLBI study, patients who lost an average of 10% of their body weight saw their sleep apnea scores improve by 31% — and tongue fat reduction was identified as the primary driver of that improvement.

So the doctors are still saying it: lose weight if you’re obese. It may be the single most impactful thing you can do for your sleep apnea — and for your life insurance premium.

Are There Any Permanent Cures For Sleep Apnea?

Potentially, yes — depending on the cause and severity. Options include oral appliances, positional therapy, radiofrequency ablation, and various surgical procedures. Most physicians agree that for long-term structural correction, surgery offers the best chance of a true cure. But ALL sleep specialists agree: the #1 first step is losing weight if you are obese.

In the opinion of world-renowned sleep surgeon Dr. Kasey Li of Palo Alto, CA, a functional “cure” requires:

- Improvement in quality of life with reduction of sleep apnea symptoms

- Achieving RDI less than 20 and reducing RDI by greater than 50%

- Improvement of oxygen nadir to 90% with few desaturations below 90%

- AHI of less than 5

In the words of Steve Lamberg, DDS, DABDSM:

“What is a ‘cure’? My answer is…That Depends. We are in the age of precision medicine. Where is the point of collapse of the airway causing the problem? We need to treat the cause. We need to move ‘airway’ treatment to the next level.”

New Sleep Apnea Treatment Breakthroughs — 2025/2026

Neuromodulation Treatment — Now Significantly Upgraded

The Inspire Upper Airway Stimulation system has received a significant upgrade. In August 2024, the FDA approved the Inspire V therapy system, the next-generation neurostimulator featuring Bluetooth connectivity, an updated patient remote, a physician programming app, and an internal sensor expected to reduce operating room time. The full commercial launch rolled out in 2025, with clinical outcomes data published at the ISSS/AAO-HNS meetings in October 2025 showing patient adherence of over six hours per night.

For patients who can’t tolerate CPAP, Inspire works by sensing when you inhale and delivering a mild stimulation to nudge the tongue forward — clearing the airway obstruction. Think of it as a pacemaker for your airway. The latest version also expanded eligibility, now covering patients with AHI up to 100 and BMI up to 40.

And Inspire isn’t alone anymore. In August 2025, the FDA also approved Nyxoah’s Genio hypoglossal nerve stimulation system — another implantable device that works regardless of sleeping position, which matters since patients spend 35–40% of their night on their back.

Life insurance implications of neuromodulation: Your broker will need to educate the underwriter with a strong cover letter and supporting clinical literature on these devices. In my experience, well-treated patients using these systems should be viewed favorably — but documentation is everything.

Surgical Procedures For Sleep Apnea

CPAP is always the first-line treatment for sleep apnea. Oral appliance therapy is a strong alternative for mild to moderate cases. Surgery is generally considered when other treatments fail, and it may be a multi-step process. The AASM published updated surgical referral guidelines to help clinicians identify the best candidates for each procedure.

Surgical Options Include (courtesy of AASM):

- Uvulopalatopharyngoplasty (UPPP) — Removes and repositions excess throat tissue; most common soft palate procedure, though rarely a standalone cure for moderate-to-severe OSA

- Radiofrequency Volumetric Tissue Reduction (RFVTR) — Uses controlled cauterization to shrink tissue in the throat; good option for mild-to-moderate OSA

- Septoplasty and Turbinate Reduction — Opens nasal passages to improve airflow

- Genioglossus Advancement — Moves the tongue attachment forward to open the airway behind the tongue

- Hyoid Suspension — Pulls the hyoid bone forward to enlarge the lower throat breathing space

- Midline Glossectomy and Lingualplasty — Removes part of the back of the tongue; uncommon but effective in select cases

- Maxillomandibular Osteotomy (MMO) and Advancement (MMA) — Moves the upper and/or lower jaw forward; best option for severe OSA

- Palatal Implants — Small fiber rods stiffen the soft palate; useful for mild apnea and snoring

- Weight Loss Surgery — Bariatric surgery can dramatically improve or resolve sleep apnea in obese patients

- Laser-Assisted Uvuloplasty (LAUP) — Not routinely recommended; less effective than UPPP

- Tracheostomy — Drastic and effective; reserved for rare, emergency situations

If you think you may need surgery, find a board-certified sleep medicine physician at an AASM-accredited sleep center near you

For Our Military Friends — VA Sleep Apnea Rules

(The Military Won’t Kick You Out, But They Won’t Let You In!)

If you’re currently active duty, the military is responsible for treating OSA like any other illness — and you’ll generally remain eligible to serve in your MOS if you’re not in a deployed or hazardous duty situation. The real challenge begins when you leave service.

A 2024 study found that 69% of OEF/OIF/OND veterans presenting to VA outpatient PTSD clinics screened as high risk for sleep apnea — compared to rates of 61–67% in similar earlier studies. Next to truck drivers, veterans remain one of the highest-risk groups for sleep apnea in the country.

How Does The VA Diagnose Sleep Apnea?

To receive a valid sleep apnea diagnosis for compensation purposes, the VA requires a formal sleep study. If you were previously diagnosed without a polysomnography study, the VA will not count that diagnosis for benefit eligibility — though they have a duty to assist you in scheduling one.

One important exception: veterans who have been service-connected for sleep apnea for at least 10 years do not need to undergo a new sleep study to maintain their rating.

Sleep Apnea Secondary To PTSD Is Huge!

PTSD remains by far the most common secondary connector to sleep apnea for veterans. According to VA Board of Veterans’ Appeals case decisions from 2025, PTSD and OSA have a recognized synergistic relationship — each condition worsens the other, and PTSD can actively interfere with CPAP therapy by triggering claustrophobia.

“Both disabilities manifest with symptoms that negatively impact the Veteran’s sleep… PTSD interferes with CPAP treatment and in that way worsens the disability.”

— VA Board of Veterans’ Appeals, 2025

That’s why it’s vital to consult a sleep doctor either while you’re in service or shortly after separation. All service members are eligible for strong benefits, and a service-connected sleep apnea disability rating can provide meaningful monthly compensation.

The VA Rating For Sleep Apnea:

- 0% — Sleep apnea documented, no symptoms requiring treatment

- 30% — Persistent daytime hypersomnolence

- 50% — Requires use of breathing assistance device (CPAP)

- 100% — Chronic respiratory failure with carbon dioxide retention, cor pulmonale, or requiring tracheostomy

Bonus Section: Sleep Apnea And Car Insurance

Is Life Insurance Directly Related To Car Insurance?

Not exactly — but if you rack up traffic violations, both your car insurance and your life insurance will cost you more. Life insurance underwriters use what’s called “lifestyle underwriting” — reviewing your driving record alongside your medical history. If they see a stack of tickets combined with untreated sleep apnea, they will likely decline to offer you a policy.

Research confirms that people with sleep apnea are significantly more likely to fail driving simulator tests and report nodding off while driving. Twenty-four percent of those with untreated sleep apnea failed standardized driving simulator tests. People with sleep disorders showed higher risk for unprovoked crashes and difficulty following basic driving instructions.

Driving with untreated sleep apnea is like driving while drunk. It’s that serious — and insurance companies know it.

Let’s Face It — Getting Life Insurance With Any Medical Condition Is Confusing

But there is an excellent life insurance policy out there for you — even with sleep apnea.

By paying attention to this guide, understanding your condition, and knowing what life insurance companies are looking for, you’ll be miles ahead on the road to affordable, high-quality sleep apnea life insurance.

Enjoy, learn, and share this resource with those you care about.

Take Action!

If you have any questions or would like to discuss your situation in more detail, please feel free to call or run quotes on the sidebar and we will respond immediately.